Research Note: Rise of Boutiques

Published April 2023

Rise of the Boutique Investment Bank

Summary of Main Takeaways

- Studies demonstrate that buyers represented by boutique banks in M&A transactions benefit from greater returns than buyers represented by full-service, bulge-bracket banks

- Specialized industry-specific boutiques can reduce information asymmetry by utilizing their superior industry knowledge

- Boutiques are segmented into three categories: Scaled / National, Industry-Specific, and Regional

- Clients today favor independent boutique advisors over large bulge brackets; independent investment banks’ M&A market share has risen from 9% in 2005 to 17% in 2019

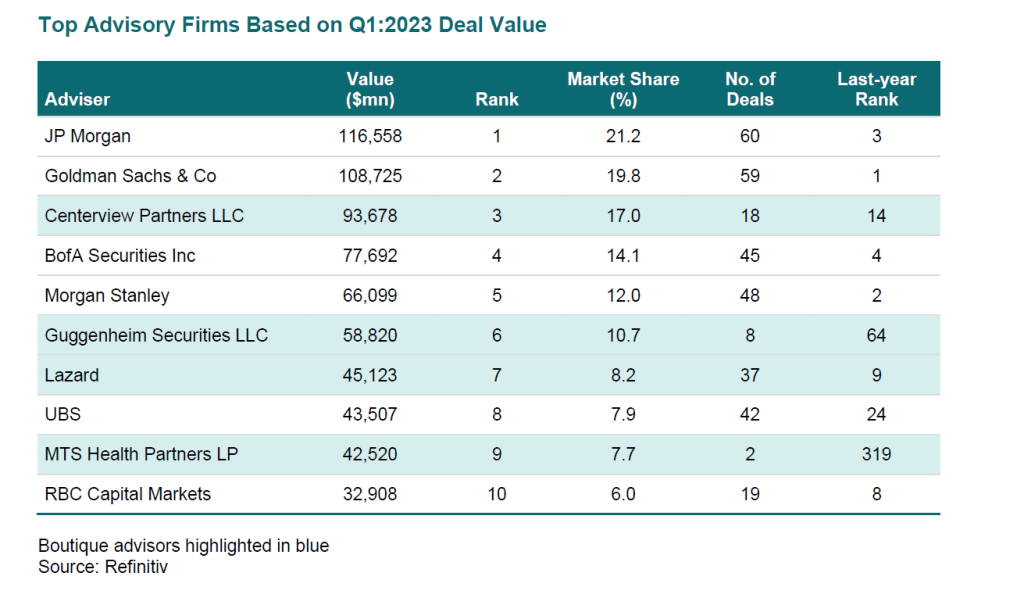

- Q1:2023 M&A league tables (see appendix) show boutiques continue to take market share from larger players; 4 out of 10 top advisors by Q1 deal volume are boutiques

Preface

Boutique investment banks are modeled on the ‘old school’ investment bank partnership model. Since Wasserstein Perella & Co was created in 1988, boutique firms have been taking market share from bulge bracket and middle market investment banks. The appeal of boutique investment banks is the independent nature of the advisory services they provide to their clients. Unlike bulge bracket banks, which are interested in providing ‘staple’ financing and other capital markets services as well as advisory, boutique investment banks focus exclusively on advisory services, whether in a particular industry, a particular investment banking product (primarily mergers and acquisitions), or a specific geography. Demand for boutique advisory services increased significantly following the Great Financial Crisis, when Lehman Brothers went under and many other bulge bracket investment banks required government bailouts as a result of their ancillary services and toxic balance sheets. As a result, bulge bracket and other larger firms saw a loss of public trust and increased government regulation via the Dodd-Frank Act of 2010. By contrast, boutique investment banks escaped with their reputations intact and their regulatory environment unchanged.

Development of the Modern Boutique Investment Bank

Boutique investment banks trace their roots to 1988 with the establishment of the first prominent boutique investment bank, Wasserstein Perella & Co. The sub-industry’s ascendance to a legitimate competitive threat to bulge bracket investment banks began in the 1990s and was cemented in the wake of the Great Financial Crisis, which drew scrutiny towards the potential conflicts of interest between large firms’ advisory and trading divisions. During the period beginning in 2000 and ending in 2016, boutique investment banks have served as financial advisors on deals totaling approximately $2.3 trillion.[1]

Much of boutique investment banks’ growth over the past two decades has resulted from both macro- and micro-level factors. On a macro-level, changes in the economy, government regulation, and industry competition have weighed more heavily on bulge bracket banks than boutique banks. On the economic front, the bursting of the tech bubble in the early 2000s and the Great Financial Crisis shifted the balance of the absolute number of deals from mega-mergers to smaller deals, which benefitted boutique banks’ ability to compete for transactions.[2] Largely because of economic developments, the regulatory environment for bulge bracket banks has become more intrusive. The Dodd-Frank Act of 2010 and the Basel Accords forced banks to increase their liquidity and tier-one capital ratios, as well as created conditions that forced full-service banks, including investment banks, to become holding companies.[3] Finally, a combination of the economic turbulence and the resulting regulatory changes facilitated an increased capacity for boutique investment banks to compete for a bigger piece of the financial advisory market, drastically increasing competition.[4]

On a micro-level, boutiques’ independence from conflicts of interest[5], specialized knowledge of a particular industry, product, or geography, and decreasing demand from clients for financing from bulge bracket banks have boosted boutiques.[6] All of these characteristics were amplified during the financial crisis when bulge bracket banks’ conflicts of interest became a point of concern for both regulators and clients. Regulators tightened the screws on bulge bracket investment banks, and clients reconsidered bulge bracket banks’ priorities and loyalties.

Avoiding the fallout of the 2008 financial crisis helped boutique investment banks boost their brands and secure long-lasting relationships with large, blue-chip clients. One example of this is Centerview’s relationship with Pfizer. Centerview’s healthcare practice was founded in 2009 by two senior bankers from Merrill Lynch, including the firm’s head of Americas M&A. The founding members brought relationships with Pfizer and numerous other blue-chip pharmaceutical clients; since then, Centerview has advised on transactions worth over $100 billion involving Pfizer (>$350 billion in healthcare transactions overall), and the pharmaceutical giant remains a close relationship to this day.

Contemporary boutique investment banks target deals of all sizes, with smaller, regional players typically advising on $10 million to $100 million transactions and larger, scaled national boutiques reaching the highest tiers of M&A (Allen & Co., a technology-focused boutique investment bank was a lead advisor to Time Warner on its $85 billion sale to AT&T in 2018, and the lead advisor to Discovery on its subsequent $43 billion acquisition of Time Warner in 2021). Additionally, boutique investment banks are prominent in private deals, which are characterized by higher information asymmetry, which leads to a need for the greater sector expertise and due diligence that boutique investment banks can provide.

As a result of these inherent business model advantages enjoyed by boutique investment banks, studies have demonstrated that buyers represented by boutique banks in M&A transactions benefit from greater returns than buyers represented by full-service, bulge-bracket banks.[7] Boutiques’ independence and superior performance combined with an increase in the number of buyers whose funding is not dependent upon full-service banks[8] has resulted in a shift in client preference to have boutiques involved in their M&A transactions.

Proof of clients’ preferences for boutique involvement can be gleaned from the fact that independent investment banks’ market share in the M&A fee pool has jumped from 9% in 2005 to 17% in 2019[9]. On top of sustained success in taking transaction market share, boutique banks are also retained by previous clients more often than their bulge bracket counterparts.[10]

Overview of Boutique Investment Banks

Boutique investment banks, like their bulge bracket counterparts, are classified into different categories. Depending on such characteristics as the number of products offered, the deal values pursued, and the geographic footprint of a bank, boutiques can be classified into one of the following categories:

- Scaled / National

- Industry-Specific

- Regional

Scaled, national boutique investment banks are characterized by:

- Transactions valued at $1 billion-plus

- The provision of more than one investment banking product, but less than what full-service banks offer

- Focus on more than one industry

- Maintenance of several offices but not worldwide coverage

Industry-specific boutiques engage in advising companies in a specific industry in which they have a high-level of intelligence and significant expertise. Due to their expertise vis-à-vis their counterparts in other banks, they are able to work on larger deals on par with their scaled / national boutiques. Their expertise and clientele also make them attractive targets for takeovers by larger, full-service banks looking to expand their presence in a specific industry vertical. An example of this kind of transaction is Piper Sandler’s 2020 acquisition of Valence Group, a chemicals-focused investment bank that became the core of the firm’s chemicals advisory group.

Regional boutique investment banks are smaller banks typically with up to one or two offices that focus on smaller deals in a particular geography in which they have intimate knowledge. Regional boutiques’ superior geographic knowledge allows them to provide robust advisory services to smaller businesses that larger banks and other boutiques could not.

Evolve Capital’s Analysis and Future Insight

Evolve Capital Partners (Evolve), with its focus on the convergence between finance and technology in the Insurance, Capital Markets and Lending verticals, falls into the category of industry-specific boutique bank. In its first decade of existence, Evolve has grown its brand and customer base and is primed for significant growth moving forward due to its expertise in a very specific and underserved market. There are numerous investment banks covering the finance or technology sectors as a standalone, but there are few that cover the convergence of the two sectors. Evolve stepped in to fill that void, and it has reaped the benefits of being a first mover in the space. Evolve will continue to maintain its independence from conflicts of interest while growing its platform to provide cutting-edge financial advisory services to its client base.

APPENDIX

REFERENCES

George Alexandridis, Nikolaos Antypas, and Vicky Lee. “Do Boutique Investment Banks Have the Midas Touch? Evidence from M&As.” (2021).

Dutta, Rajib, Bulge Bracket and Boutique Advisory Banks (A Conceptual Study) (May 7, 2022). Journal of Commerce & Accounting Research, 11 (2) 2022, 94-105 http://publishingindia.com/jcar/47/bulge-bracket-and-boutique-advisory-banks-a-conceptual-study/31970/76521/, Available at SSRN: https://ssrn.com/abstract=4102350

Ivan Levingston, Sujeet Indap, and James Fontanella-Khan. “Boutique adviser Centerview beats Wall Street banks in deal rankings.” (2023)

[1] George Alexandridis, Nikolaos Antypas, and Vicky Lee, p. 1.

[2] George Alexandridis, Nikolaos Antypas, and Vicky Lee, p. 11.

[3] George Alexandridis, Nikolaos Antypas, and Vicky Lee, p. 11.

[4] George Alexandridis, Nikolaos Antypas, and Vicky Lee, p. 11.

[5] Boutique investment banks traditionally focus on advisory services, but some of the larger scaled boutique investment banks have established equity research capacities.

[6] Rajib Dutta, p. 1.

[7] George Alexandridis, Nikolaos Antypas, and Vicky Lee, p. 1.

[8] George Alexandridis, Nikolaos Antypas, and Vicky Lee, p. 9.

[9] Ivan Levingston, Sujeet Indap, and James Fontanella-Khan

[10] George Alexandridis, Nikolaos Antypas, and Vicky Lee, p. 4.