Research Note: 2024 Outlook

2024 Macroeconomic Outlook

EXECUTIVE SUMMARY

Evolve Capital Partners (“Evolve”) is pleased to present our January 2024 Executive Research Note, highlighting the sustained impact of market trends on our core coverage areas: Insurance and Capital Markets. The year 2023 concluded with stable interest rates and a positive market trend, alongside moderating inflation.

The ripple effects of recent years’ interest rate increases are still permeating the market, but their influence on M&A activity is expected to persist throughout 2024. While we do not anticipate a decline in rates, their stability should drive increased transaction activity, coupled with increased labor productivity. This is (hopefully) reminiscent of the healthier M&A and transaction environment observed in the mid-1990s to early 2000s. We foresee a rise in transactions in the latter half of 2024, highlighting the importance of current strategic planning.

In the Insurance vertical, we expect the hardening market to persist. Investors and buyers are likely to continue seeking quality and stable firms, with a particular focus on services and claims firms, especially within the highly fragmented Third-Party Administrator (TPA) space.

The Capital Markets vertical is positioned for continued consolidation among alternative asset managers, with a new “small” wave of IPOs expected in 2024. This trend should help mitigate the industry-wide reductions in workforce.

Key Takeaways

- Interest Rates and Market Stability: The stabilization of interest rates creates a more predictable environment for M&A activity in 2024, hopefully reminiscent of the stability seen in the mid-1990s to early 2000s. We expect an increase in transactions, especially in the second half of the year.

- Insurance Vertical Dynamics: The insurance sector’s hardening market continues, with a focus on acquiring quality and stable firms. The fragmented nature of the TPA space is particularly conducive to transaction activity.

- Capital Markets Trends: Ongoing consolidation in alternative asset management, coupled with an expected new set of IPOs in 2024, will likely counterbalance workforce reductions and strengthen the sector.

In Evolve’s January 2023 research note, we predicted continued monetary tightening and the impact of claims inflation on insurance margins, requiring further pricing increases. Our emphasis on the significance of size and AUM for alternative management companies was also validated, as firms are beginning to consolidate. Reflecting on 2022, we recognized that prevailing inflation was primarily supply-driven, and the observed interest rates marked a return to the economy’s historical norms, a perspective that has gained increasing validation.

If you’re contemplating a transaction in our verticals, whether it’s a sale or capital raise, 2024 is shaping up to be a return to hopefully a more normal environment, akin to what 2020 should have been. This period is expected to see a reopening of market activities, with buyers and sellers finding common ground on valuations. Additionally, the process of assessing risks is anticipated to become clearer, facilitating transaction processes and leading to higher closing rates.

BIG PICTURE

Market Returns in the Insurance and Capital Markets Verticals

The market performance in 2023, especially in the S&P 500 and financial sectors, indicates a significant shift towards recovery or stabilization, despite earlier challenges. The S&P 500 outperformed projections with a 24.23% return, while the financial sector and specific indices like the Dow Jones US Select Insurance and Investment Services Indexes also showed strong performances.

Looking ahead, the high volume of cash-like assets held by institutions and investors, amounting to $5.7 trillion, is a positive indicator for the public markets. This reserve, combined with an improving inflation outlook, suggests potential growth and stability in stocks and bonds. As companies align with their earnings projections, the market should hopefully deliver relative clarity, providing a favorable environment for founder-run firms to evaluate and maximize the value of their businesses. This evolving landscape offers a promising outlook for the insurance and capital markets verticals in the coming year.

Market Valuations and Financial Services Indices:

The S&P 500’s performance in 2023 was solid. Initially projected to end the year with a 9.4% increase, it actually returned 24.23%, indicating strong market recovery.

- The S&P Financial Sector yielded a return of approximately 9.9% in 2023.

- The Dow Jones US Select Insurance Index returned 11.66% in 2023, compared to 11.94% in 2022, with a trailing P/E of 22x and a forward P/E of 13.66.

- The Dow Jones US Select Investment Services Index in the Capital Markets returned 15.48% in 2023, a significant rebound from (10.36%) in 2022, with a trailing P/E of 28x and a forward P/E of 24x.

Valuations:

The S&P 500’s Price to Earnings Ratio remained strong at the end of 2023. The Forward Estimate PE Ratio was about 24.7x, above the average ratio since 1981 of 21.2x. This could suggest a 20% market overvaluation, unless companies grow into their earnings projections, leading to a relatively stable market.

Future Outlook in Public Markets:

Institutions and investors are holding a record $5.7 trillion in cash-like money-market funds, many yielding above 5%, per the Wall Street Journal. This is seen as a bullish signal for stocks and bonds, especially if the inflation outlook continues to improve.

Transaction Activity and Deal Dynamics

In 2024, M&A activity is not anticipated to rise immediately, but a gradual increase is expected. The low number of transactions in 2023 sets a lower benchmark for surpassing year-over-year comparisons in 2024. Challenges remain, particularly in the U.S., where large deals face antitrust scrutiny, but the market is poised for recovery due to stable economic conditions and halted rate hikes by central banks. Although IPO activities are likely to increase from 2023, a large rise in new offerings isn’t anticipated, and top-tier private companies may delay public listings until at least 2025.

Private equity is seeing a downturn in acquisitions and exits, reaching a 30-year low, leading to longer holding periods for portfolio companies and a potential slowdown in LBO fundraising. Despite this, there’s a notable increase in PE investments in the insurance technology sector. Founder-owned firms are experiencing a rise in acquisitions by PE groups, reflecting a shift in the investment landscape and providing opportunities for smaller-scale transactions.

View on M&A and Possible IPOs in 2024

- The upcoming year is expected to see a rise in M&A activities within the fintech and insurtech sectors.

- IPO activity in 2024 may exceed that of 2023, but a rise of new offerings is not anticipated. It’s likely that the IPOs that do occur will be down-round, with complex capital structures.

- Top-tier private companies might postpone their public listings until at least 2025, to align with their 2021 valuations.

Private Equity: Pullback on Acquisitions & Exits

- The exit activity in private equity has seen a decline, reaching its lowest level in three decades. This trend is leading to prolonged holdings of portfolio companies, impacting distribution rates for general partners and potentially slowing down fundraising efforts for LBO strategies.

- Private equity firms, previously active in buying insurance brokerage businesses, have seen a decrease in deal numbers in recent quarters.

- The middle market in private equity has experienced a decrease in deal volume and exit value, with contracting multiples for transactions targeting small to medium-sized companies.

View on Capital Raises in 2024

- Insurtech is experiencing a revival, as evidenced by an uptick in venture capital investment. In the third quarter, there was a 53% increase in VC funding for insurtech startups, totaling $1.7 billion across 115 deals. This marks a notable turnaround for the sector, which had been on a decline since 2021, according to data from Pitchbook.

- Private equity firms have increased their investment in the insurance technology sector, surpassing the previous year’s total. In the first three quarters, PE firms invested $6.8 billion in insurtech, overtaking the $4.2 billion total of 2022, as reported by Pitchbook research.

- Fundraising by US venture capital firms has reached a six-year low, indicating a challenging environment for startups.

- However, convertible debt issuance has seen a notable increase of 77% last year to $48 billion, offering substantial interest rate savings, according to LSEG data.

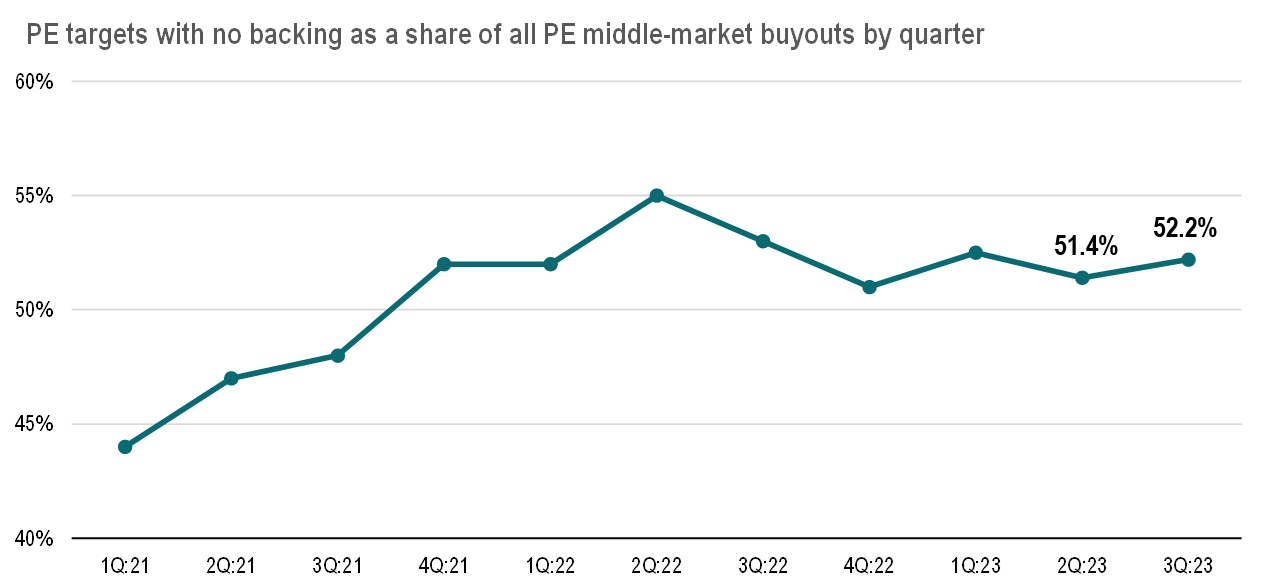

Impact on Founder-Owned Firms

- Acquisitions of non-backed firms by private equity groups are on the rise, marking a shift in the market landscape.

- These transactions, typically smaller in scale, usually range between $25 million to $100 million and often include deals below $25 million. They tend to be discounted compared to larger, sponsor-backed transactions. In larger segment of the middle market (above $100 million), the median Trailing Twelve Months (TTM) EV/EBITDA multiple stands at 11.4x, which decreases to 6.8x for deals under $100 million. Similarly, the EV/revenue multiples also reduce from 2.4x to 1.1x within this size range, as per Pitchbook data.

Source: PitchBook

Macro Trend Impacts on M&A in the Insurance and Capital Markets Verticals

In 2023, the U.S. insurance and capital markets sectors experienced varied M&A activities due to economic fluctuations. Certain areas in the insurance vertical saw continued M&A interest, with strong demand in insurance brokerage despite inflation and rate hikes. The insurance services sector remained stable, with a trend toward specialized claims firms, agents and underwriters. The capital markets vertical saw potential for new IPOs and continued consolidation in alternative investments; however, BPO in capital markets remained strong.

Impact on the Insurance Vertical:

- In 2023, the U.S. insurance sector’s M&A activity navigated a complex environment, influenced by fluctuating economic conditions. The year began positively, indicating robust M&A interest despite economic uncertainties.

- However, as the year progressed, challenges arose from conflicting economic projections, inflation, and Federal Reserve’s interest rate hikes. Nonetheless, the insurance brokerage sector maintained strong demand and high valuations.

- For 2024, the trends from 2023, especially the strong Q4 in insurance brokerage M&A, suggest continued active M&A in this sector.

Insurance Services:

- M&A activity in the U.S. insurance services sector in 2023 was relatively stable compared to 2022, with deal values approximately half of the previous period. The sector saw almost 310 insurance transactions with over $11 billion in deal value from during the last three quarters of 2023 according to Deloitte.

- Projections for 2024 indicate active deal-making, with insurance distributors remaining attractive to consolidators and private equity firms. The current interest rate environment has not significantly impacted valuations in this subsector.

- A trend towards specialty managing general agents and underwriters (MGAs and MGUs) continues, driving divestitures and expected to persist into 2024. The trend of agency acquisitions persisted, with 751 deals announced. Notably, EBITDA multiple valuations experienced an increase in 2023, reaching 14.9x, as reported by Marsh Berry.

Insurance Software:

- InsurTech companies led acquisition activity in 2023 as carriers sought point solutions for transformation initiatives. While 2024’s M&A market could remain muted, low valuations and financial challenges for start-ups could increase deal volumes, particularly in areas like AI, blockchain, and cloud computing.

Impact on the Capital Markets Vertical:

New Small Wave of Potential IPOs: 2024 may see a surge in IPOs within the capital markets, as asset management firms seek public listing to obtain liquidity in a tough capital-raising climate.

- Diversification and Expansion: Firms are increasingly diversifying into new strategies like private debt and exploring new geographic markets, following a trend among large fund managers to raise larger vehicles.

- Consolidation in Alternative Investments: Prominent firms, including CVC Capital and General Atlantic, are considering public listings, indicating significant consolidation efforts.

- Strategic Partnerships: BlackRock’s negotiations with Warburg Pincus, while now dead, underline the dynamic nature of the private funds industry, with a focus on transformative deals and joint ventures.

Capital Markets Services:

- In 2023, M&A activity in the Business Process Outsourcing (BPO) sector, particularly in capital markets, remained strong despite economic volatility. The sector saw sustained M&A volumes.

- This activity was increased by a well-capitalized buyer base and private equity firms with substantial resources. Expansion in service offerings by sector participants attracted acquirer interest, especially in the BPO market.

- Looking into 2024, the capital markets services sector’s outlook is shaped by factors such as the need for growth, innovation, demand for advanced technologies like AI, and a changing regulatory landscape, influencing M&A activities.

Capital Markets Technology:

- M&A activity in the U.S. capital markets technology sector experienced a slowdown in early 2023 but rebounded in the latter half of the year. Despite the increase in deal volume, overall deal values stayed below past averages, indicating transactions at lower valuations.

- For 2024, the M&A market is expected to be suppressed. However, persistent low valuations and financial challenges facing startups could lead to an increase in deal volume, though at lower prices.

Interest Rates & Monetary Policy

Most major central banks are expected to have concluded their rate hiking cycles. As interest rates stabilize, these central banks are likely to maintain policy rates above their long-term sustainable level projections. This transition to a higher interest rate environment, though challenging, presents an opportunity for better forward returns on fixed income assets, and clarity on financing availability for transactions.

- Fiscal policy in the US is likely to exert minimal drag, as most pandemic-related stimulus has ended, and significant fiscal consolidation is unlikely during a presidential election year.

- In the US, strong economic growth is expected to reduce the urgency for rate cuts, potentially delaying the first reduction until the fourth quarter of 2024.

- The year 2024 is poised to reinforce the view that the global economy has moved beyond the post-Global Financial Crisis era characterized by low inflation, zero policy rates, and negative real yields.

- Currently, policy rates are positive in most regions, and real yields have returned to pre-GFC levels, minimizing concerns about deflationary risks, according to Goldman Sachs.

GDP Growth

The global economy in 2023 surpassed most everyone’s most optimistic expectations. According to Goldman Sachs, global GDP growth is set to exceed consensus forecasts from the previous year by 1%, with the US outpacing this by achieving a 2% increase.

- Concurrently, core inflation has reduced from 6% in 2022 to 3% across economies that experienced post-COVID price surges.

- Looking ahead, further disinflation is anticipated, per Goldman Sachs. Although product and labor markets have substantially normalized, the complete effects of disinflation are still unfolding.

Regulatory Impacts

Insurance Sector:

Climate Change: The sector faced enhanced climate risk disclosure and management requirements. The Securities and Exchange Commission (SEC) is developing guidelines for emission reporting, with further regulatory developments expected in 2024.

- AI and ML: Insurers are integrating AI for roles such as actuaries and claims adjusters, but regulatory concerns necessitate careful implementation and quality control.

- Cybersecurity: Increased digitization led to stricter regulatory demands for enhanced cybersecurity measures and rapid disclosure protocols.

Capital Markets / Lending:

Divergent Regulations: Varied international laws, especially in the EU, continue to impact areas like crypto, digital assets, AI, and climate risk, with a focus on consumer protection and industry resilience.

- Capital Requirements: Banks in the US may face tighter capital rules under Basel III reforms starting in 2025, impacting their capital markets activities and lending capabilities.

- Regional and Small Banks: These institutions face intensified regulatory pressure, leading to efforts to diversify portfolios and tighten lending standards.

- Wealth Management: The SEC is proposing rules to prioritize investors’ interests, particularly in the use of AI.

MACRO TRENDS IMPACT ON EVOLVE’S VERTICALS

Insurance

In 2023, the P&C insurance sector had a rise in climate-induced disasters, leading to significant losses and a shift in market dynamics. Insurers retreated from high-risk areas, passing the burden to state-backed insurers, and faced soaring reinsurance costs. The sector experienced increased premiums, notably in commercial property and personal lines. The specialty insurance market is projected to grow significantly by 2024. Life insurance premiums remained strong in 2022 despite a coverage gap. The Life and Annuity sector anticipates diverse growth patterns and digital transformation challenges. Insurers are increasingly adopting advanced technologies for efficiency and customer engagement, with a focus on claims automation and partnerships with InsurTech firms.

P&C

- Climate Change Impact on P&C Insurance: The insurance industry in 2023 saw a surge in climate change-induced extreme weather events, leading to more billion-dollar disasters than any year on record by the National Oceanic and Atmospheric Administration. This resulted in substantial losses, particularly in high-risk areas like Florida, where hurricane damage cost up to 10% of the state’s GDP.

- Market Response and Reinsurance Trends: In response to these challenges, private insurers retreated from risky markets, shifting the burden to state-backed insurers offering less coverage at higher prices. Property reinsurers resisted lowering prices, which led to increased affordability pressures. The property-catastrophe reinsurance costs for primary non-life carriers jumped by 30.1% in 2023, a significant rise from the previous year’s increase, according to Deloitte.

- Rising Insurance Rates and Costs: The insurance sector experienced rising rates, with commercial property premiums increasing by an average of 20.4%—the first time since 2001 that rates rose above 20%. Inflation eased somewhat in 2023, but insurance rates continued to rise, particularly in areas like property coverage. The personal lines insurers also faced rising costs, with auto carriers seeing a 20.2% increase in vehicle repair costs compared to a 15.5% increase in premiums.

- Growth in Specialty Insurance Market: The specialty insurance market, driven by persistent hard market conditions, InsurTech innovation, and the increasing frequency and severity of catastrophes, is projected to grow from $81.5 billion in 2022 to an estimated $130.1 billion by 2024, at a compound annual growth rate of almost 10%. Europe was the largest region in this market in 2022.

Life Insurance

- 2022 Premium Growth: U.S. life insurance premiums reached $15.3 billion in 2022, on par with the record highs of 2021. This growth occurred despite over 100 million U.S. adults living with an insurance coverage gap.

- Sales Deceleration: Sales slowed in the latter half of the year, influenced by consumer concerns over inflation and economic uncertainties, even as COVID-19 worries diminished.

- Global L&A Sector Divergence: The Life and Annuity (L&A) sector is expected to experience divergent growth patterns between advanced and emerging markets through 2023-2024.

- Sector Transformation: L&A carriers are adapting to increased digitalization and evolving customer expectations for more relevant and comprehensive product offerings. This strategic shift is aimed at achieving more predictable and sustained growth amid economic, environmental, and societal changes.

- 2024 Sector Outlook: The year 2024 is poised to be pivotal for the sector, with insurers considering transformative steps to address both market demands and external pressures, despite challenges from legacy systems and siloed organizational structures.

Technology Impacts

- Evolving Operating Environment: Insurers face increased pressure to adopt automation, AI, and advanced analytics to adapt to the rapidly changing environment and improve their core operations.

- Operational Efficiency and Client Services: Advanced technologies enable more accurate underwriting, effective claims management, and operational streamlining. They also foster proactive risk mitigation, personalized services, and outreach to underserved segments.

- Digital Transformation Demand: Despite ongoing digital transformation efforts, there is still a need for services, interfaces, and experiences on par with sectors like e-commerce.

- Overcoming Legacy Constraints: Challenges from outdated systems hinder experience optimization. Insurers are encouraged to enhance customer interfaces with engaging AI and analytics-driven solutions.

- Claims Automation: Insurance companies are balancing automated claims processing with personalized service, using technology to enhance decision-making and reduce costs.

- Collaborations with InsurTechs: Partnerships between established insurers and InsurTech firms are growing, aiming to create innovative solutions and accelerate industry innovation.

- Digital Distribution Channels: The rise of online marketplaces and aggregators continues, with embedded insurance products simplifying the purchasing process and potentially increasing customer engagement.

Capital Markets / Lending

In 2024, investment banking is anticipated to grow modestly, driven by restructuring in CRE and technology sectors, alongside refinancing and sustainability initiatives. The use of generative AI is set to enhance efficiency and market positioning. In wealth management, global wealth continues to rise, with a significant increase in technology use for personalized services and automation. Banking sees steady commercial loan growth but faces risk management challenges, with digitization being a key focus. Traditional exchanges are adapting to intense competition and technological advancements, pursuing strategic acquisitions for revenue diversification and focusing on global investor attraction strategies.

Investment Banking & Corporate Advisory

- Investment Banking Growth in 2024: Anticipated modest growth with a focus on restructuring services, especially in the CRE and technology sectors. This growth is expected to be driven by refinancing and sustainability-led initiatives, enhancing advisory and issuance revenues. The trading arm, however, might see limited growth due to persisting lower volatility.

- Generative AI and Market Dynamics: Investment banking is turning to generative AI to boost efficiency and stand out in a competitive market. This technology, along with the focus on large-scale operations, will benefit major players, while smaller firms will need to specialize and adapt strategically.

- Underwriting and Advisory Business: The sector is poised for continued growth, driven by stronger market sentiment and an increased demand for IPOs and equity issuances. A rising backlog of deals, particularly in the U.S., is expected to stimulate deal and issuance activity in various sectors.

- Private Capital and Workforce Trends: Private capital is emerging as a significant player, competing with traditional banks in lending and trading activities. US private markets raised over $250 billion capital in 2022 according to JP Morgan. Despite recent workforce reductions in global banks, there’s an optimistic outlook for a resurgence in deal-making activities. The adoption of AI in areas like coding could provide cost-saving opportunities.

Wealth and Investment & Asset Management

- Global Wealth Growth: Despite market volatility, global wealth is increasing, with a forecast to surpass $500 trillion in 2024. The Asia-Pacific region leads with about 40% of global wealth, followed by North America (33%) and Europe (23%) according to Credit Suisse.

- Technology in Wealth Management: Wealth managers are increasingly leveraging technology, particularly AI, for personalized advice and automation of routine tasks, focusing on cost rationalization and regulatory compliance.

- Investment Trends: Exchange-traded funds are preferred, but alternative investments are gaining momentum, potentially rising from 11% to 20% of household assets by 2026.

- Market Challenges: The industry faces challenges from macroeconomic, geopolitical, and regulatory uncertainties. The number of funds closed recently was the lowest since 2014, indicating a trend toward greater market concentration and bifurcation in asset manager performance.

Banking

- Banking Priorities: Corporate and transaction banks face steady commercial loan growth, tighter lending standards, and increased risk in CRE loan portfolios, prompting a focus on risk management and digitization.

- Emerging Opportunities: Growth areas include digital asset custody and green transition strategy advice, with banks needing to remain agile and adopt an advice-based model alongside self-service options.

- Risk Management Strategies: Banks should use alternative data for risk management and refine customer segmentation to tailor credit processes and risk monitoring.

- Digitization and Efficiency: There’s pressure to enhance digitization, especially using AI/ML and APIs for improved risk selection and operational efficiency in loan processing, with an emphasis on automating standard loan services.

Infrastructure for the Markets

- Intensifying Competition for Traditional Exchanges: Traditional exchanges face increasing competition from niche and regional players, with exchanges in emerging markets expected to surpass U.S. exchanges in market cap by 2030.

- Global Attraction Strategy: To remain competitive, traditional exchanges need to attract global investors through dual listings and ecosystem support.

- Profitability Challenges: Exchanges are pressured by competition from niche and emerging market trading venues, alongside client demand for diversified services.

- Technology and Data Investment: There’s a push for technological advancements to keep pace with alternative trading systems and capitalize on the growing market for real-time data and analytics. Global spend on market data approached $40 billion in 2022 according to TP ICAP.

- Strategic Acquisitions and Revenue Diversification: Major exchanges like Nasdaq are making strategic acquisitions to enhance their value propositions and diversify revenue sources, particularly in software and data services.

CONCLUDING REMARKS

As the market seeks clarity on interest rates and faces a reduced money supply, overall visibility is improving, leading to a more stable environment for deal-making.

In the insurance vertical, particularly within P&C, efforts to rework and reprice large catastrophic losses are contributing to this stability. The Capital Markets sector, still grappling with uncertainties around rates and asset values, is seeing consolidation among smaller, less profitable entities.

However, a convergence in valuation expectations between buyers and sellers is expected, signaling a move towards a more normalized transactional landscape.

The advancements in technology, which are driving efficiencies, have the potential to bring us back to an environment reminiscent of the mid-1990s to early 2000s. This era was characterized by heightened deal activity, suggesting a promising outlook for similar dynamics in the current market.

Or at least bringing us to what 2020 could (or should) have been….

References:

All sources are available upon request to the Evolve research team and market data provided by S&P.

- Deloitte: Referenced for insights on the U.S. insurance services sector in 2023, particularly regarding deal values and projections for 2024.

- Pitchbook: Cited for data on InsurTech venture capital investment in Q3, PE investment in the insurance technology sector, convertible debt issuance, and middle market deal multiples.

- Goldman Sachs: Mentioned for perspectives on global GDP growth, inflation, and deflationary trends.

- JP Morgan: Referenced in the context of private capital raised in the U.S. private markets in 2022.

- TP ICAP: Cited for data on global spending on market data in 2022.

- Credit Suisse: Referenced for insights on global wealth growth projections for 2024, including regional distribution of wealth.

- National Oceanic and Atmospheric Administration (NOAA): Mentioned in the context of climate change-induced extreme weather events and their financial impact.