Evolve Inflationary Outlook: Everything is Going to be Okay

Published September 2022

Preface

Current financial reporting is rife with stories of economic volatility and ‘the sky is falling’ predictions. However, much of the analysis being presented is superficial, exaggerated or misguided. The truth can be difficult to decipher, especially if you are considering a high impact M&A or a capital raise transaction.

Evolve Capital has taken a deep dive into the quantitative and qualitative indicators actually present in today’s markets. And our findings point to an economy that is well within normal inflationary measures and is showing clear signs of recovery from the past two years of pandemic upheaval.

Put simply, everything is going to be okay. We expect to see deal volumes and deal diligence return to normal levels following the pandemic-induced spike in 2021 and the first half of 2022.

Below, we present our research findings, focusing on our three core coverage verticals: insurance, capital markets and lending. If you operate in one of these verticals and are considering an upcoming strategic transaction (such as sale, acquisition, capital raise), most notably if it is planned for before the end of 2023, then this is crucial information that will help lead to a successful transaction.

OVERVIEW

Inflation

As has been widely reported, the inflation we are seeing in today’s economy is primarily supply driven. Supply chain disruptions caused by the pandemic are causing upward price pressures, made worse by Russia’s invasion of Ukraine which has led to shortages in oil and other commodities.

Our research has identified the following trends which indicate that inflation is already beginning to ease:

- Oil prices are ticking down, with WTI crude prices down ~35% from June’s peak (as of August 31, 2022).

- Semiconductor prices are down 14% year-on-year, a sign that semiconductor shortages are easing.

- Gold prices are at 2-year lows, currently at $1,716 per ounce, compared with $1,815 one year ago (as of August 31, 2022). Because gold is viewed as a good hedge against inflation, it tends to be priced high in times of high inflation.

- Supply chains are showing signs of improvement, with the Oxford Economics’ U.S. Supply Chain Stress Index declining for four consecutive months. Once the supply chain corrects itself, the inflation we are seeing should revert back to normal levels. (Statement by Former Fed Vice Chairman Alan Blinder here.)

- Unemployment is down to 2019 levels and long term inflation expectations are down to 2.8%, a one-year low.

Interest Rates

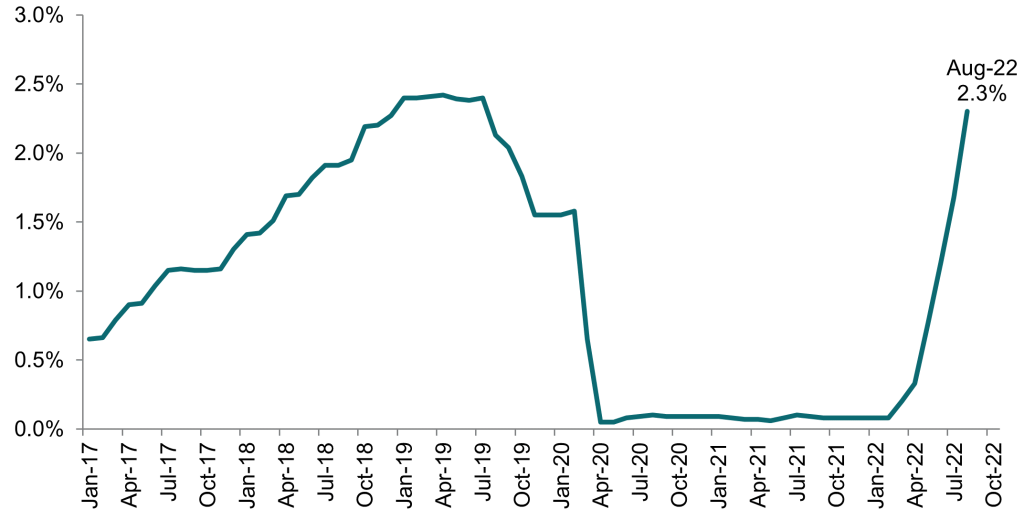

Even with the recent increase in interest rates by the Fed, current rates are still below pre-pandemic levels, as shown in Figure 1. One reason for what seems to be an over-sensitivity to interest rate increases is the fact that from 2009 to 2016, and then throughout the pandemic, interest rates were exceptionally low. The interest rates we are currently seeing are not abnormal – they are simply shifting back to where the economy once was. The recent rate hikes will also help slow inflation, but it will take time for results to show; pre-pandemic estimates suggest that anti-inflation monetary policy takes two to three years to reach its full effect.

INFLATION’S EFFECTS ON EVOLVE’S THREE FOCUS VERTICALS: INSURANCE, CAPITAL MARKETS AND LENDING

INSURANCE

Distribution Firms

Increased premiums amongst insurance carriers have directly benefited distribution firms, who have seen their commissions rise as a result. This has led to strong PE demand for broker/agency companies, with more than 75% of all broker/agency deals in 2021 involving PE funds. Some recent examples of this are Lovell Minnick Partners acquiring Warner Pacific on December 31, 2021, for an undisclosed amount (full article here), Brookfield acquiring American National for $5.1 billion (closed on May 25, 2022), implying a 0.8x March 2022 book value multiple (full article here), and Owl Rock Capital acquiring PCF for $2.2 billion on November 2, 2021, implying a 5.5x revenue multiple (full article here).

While PE demand remains strong, the supply of potential targets is falling in the distribution part of the insurance vertical, especially for niche brokerages and agencies, which presents attractive opportunities for high-quality companies to receive a high premium.

Insurance Software Firms

Given the rise in claim costs, the shift toward claim prevention has accelerated in the insurance sector. For example, Allstate has recently implemented a telematics program that provides automobile drivers with personalized driving feedback after each trip, with discounts being offered to those policy holders who demonstrate ‘safe driving’.

This shift in focus toward claim prevention and improving consumer habits benefits the software firms that are able to provide insurance companies with data-driven insights (full article here).

In cyber insurance, firms that can detect security risks early are considered valuable. An example of this is specialty insurer, HSB, who acquired Zeguro’s digital cybersecurity platform on October 21, 2021. This platform includes a suite of cyber risk management tools and services, including cybersecurity training and web application monitoring that helps businesses identify their cyber vulnerabilities (full article here).

This focus on data collection technologies is mirrored in the auto insurance sector, with Lemonade acquiring Metromile for $145 million in stock (announced on November 8, 2021 and closed on July 28, 2022), implying a 0.9x book value multiple (March 2022 book value) , in order to integrate telematics into their auto insurance offering (full article here).

Property & Casualty Carriers

With P&C carriers, rising claims costs may push combined ratios above 100%. In the auto insurance sector, the combined ratio already surpassed 100%, in 2021, and it is expected to worsen this year. As a result, many auto insurers have increased their rates substantially, some by double digits. Examples of this include Allstate, who increased private passenger auto insurance rates in Louisiana by 14.9%, and Progressive, who increased rates by 15% in Texas.

However, given that inflation is primarily a supply-side issue that we expect to revert to normal levels over the coming one to two years, we believe that there will be minimal long-term systematic risks for insurance carriers.

M&A activity in the P&C insurance sector in 2021 was higher than the 25-year inflation adjusted average. Historically, this type of elevated figure results in a cooldown in the following year. This prediction is already playing out, with approximately 200 M&A deals in the U.S. P&C space in both 2020 and 2021, and only 82 M&A deals in the first seven months of 2022.

Life Carriers

Evolve believes that Life carriers should be relatively insulated from the effects of inflation given that life carriers typically hold their bond portfolios to maturity. This means that falling bond prices (due to higher interest rates) will not lead to realized losses. Also, because their payouts are fixed, they face far less uncertainty, and therefore their margins won’t suffer.

In fact, Evolve predicts that some Life carriers will be seeing increased opportunities in the long term. The current rise in interest rates will result in higher yields on investments, which will increase margins on policies being sold today.

Overall, M&A activity in this space will be focused on lowering balance sheet risk through the divestiture of capital-intensive in-force business lines. An example of this is Allstate selling its life insurance business to Blackstone (closed on November 1, 2021) in order to deploy capital out of spread-based products (full article here).

CAPITAL MARKETS

Broker-Dealers

Evolve Capital expects the current economic environment — rising rates, rising prices and somewhat volatile market behavior — to benefit brokers with a larger proportion of experienced investors.

Conversely, we expect online brokers with a large proportion of first-time, short-term traders to be at a disadvantage given that inexperienced traders may not know how to navigate this environment, leading to lower trading volumes.

Examples of this include the success of LPL financial, the largest independent broker-dealer in the U.S. (by assets). LPL saw Q2 2022 net income increase by 35% year-on-year, and LPL stock is up 36% year-to-date (as of August 31, 2022). On the other hand, Robinhood, known for its inexperienced user-base, saw transaction-based revenue in Q2 2022 drop more than 50%, from $451 million in Q2 2021 to $202 million in Q2 2022. In fact, Robinhood was quoted as losing 34% of its monthly active users over the past year, with numbers decreasing from 21 million to 14 million (full story here).

As some firms struggle, Evolve Capital predicts some increased M&A activity as online brokers look to expand their offerings and diversify their revenue streams. An example of this is crypto exchange FTX that is reportedly looking to acquire brokerage start-ups in order to expand into stock trading (full article here) and Public.com’s acquisition of Otis on March 9, 2022, in order to expand into alternative assets (full article here).

Asset Managers

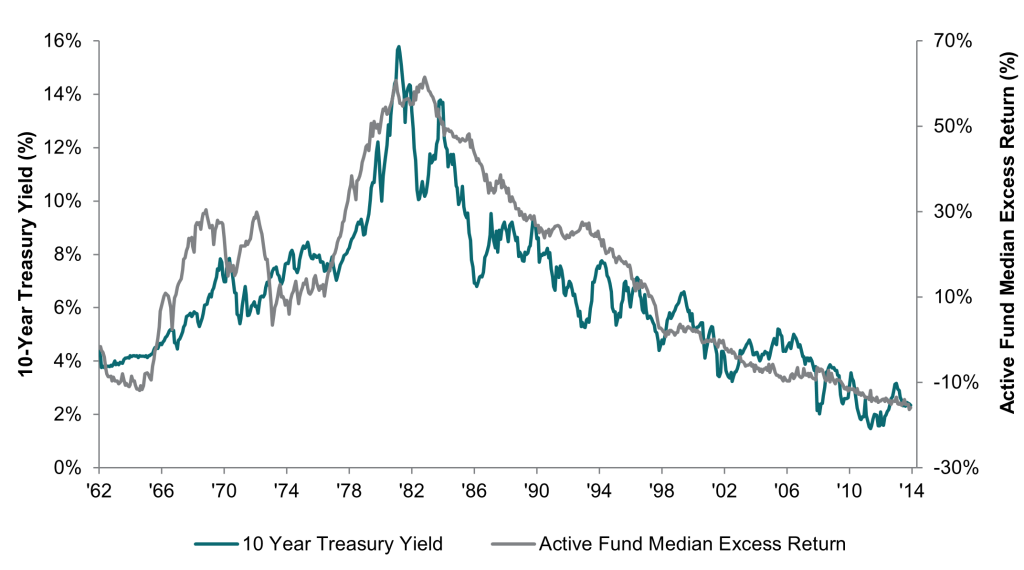

Actively managed funds have been under pressure over the last few years given that the low interest rate environment has led to high returns for passive investment strategies, thus making it difficult for actively managed funds to compete with these low-cost passive funds.

However, past data demonstrates that actively managed funds have typically done well in higher interest rate environments (see Figure 2).

Alternative strategy funds have been seeing strong inflows, which has translated into strong M&A demand. Examples of this include Alliance Bernstein’s $1.4 billion acquisition of CarVal Investors (closed on July 1, 2022 – full article here) and Franklin Templeton’s $1.75 billion acquisition of Lexington Partners (closed on April 1, 2022 – full article here).

Insurance companies and banks are also looking to enter, or re-enter, the asset management space due to its capital-light business model. Although recently terminated, UBS’ attempted acquisition of Wealthfront for $1.4 billion (announced on January 26, 2022) serves as a great example of this trend.

Instead of an acquisition, UBS invested into WealthFront at a similar valuation (full paywall article by the Financial Times here). Though financial details of the transaction were undisclosed, industry expert Michael Kitces estimates the company’s revenue at $70 million, implying a trailing 21x multiple.

Service Providers

Firms looking to decrease operating costs have led to increased demand for automation and specialized software, thus creating opportunities for service providers. An example is GemSpring’s acquisition of Goldensource on May 17, 2022 (full article here).

Evolve Capital also expects increased competition amongst broker dealers to lead to increased demand for low-cost solutions and alternative revenue streams benefiting service providers. For example, StoneCastle, which provides bank sweep solutions for broker-dealers, saw their deposits increase at a CAGR of 55% over the last five years as broker-dealers sought to receive interest income from unused cash balances. With such strong growth, Veritex a community bank, acquired interLINK, a subsidiary of StoneCastle Partners, on March 3, 2022 for $91 million in order to gain access to close to approximately $6 billion in stable deposits (full article here).

LENDING

Banks

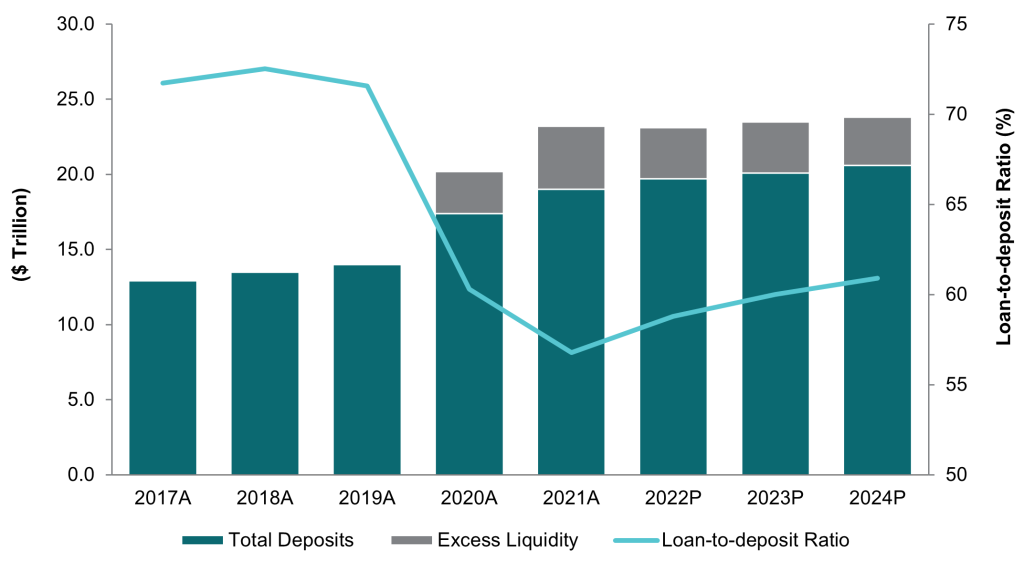

Within the banking sector, loan-to-deposit ratios are at historic lows (see Figure 3) and banks have significant excess liquidity. As a result, as interest rates rise, banks should be able to increase interest rates on loans without increasing interest rates on deposits, thereby boosting NIMs.

Banks are also increasingly digitizing, which is the result of growth in FinTechs combined with increasing business operational costs. An example of this shift is Goldman’s acquisition of Greensky for $1.9 billion (announced on September 15, 2021 and closed on March 29, 2022) (full article here). This purchase price implies a 11.9x 2021 EBITDA multiple.

Overall, the growth in bank earnings — specifically community bank earnings — is expected to decline in 2022 and into 2023, compared to 2021. For banks without strong earnings growth, a capital raise or sale may be necessary in order to fund infrastructure and digital channel improvements. Examples of this include FNB’s recent acquisition of Union Bank (40% of Union Bank’s deposits are non-interest bearing which is attractive in a rising rate environment, full article here).

Equipment Financing

The equipment financing sector should see positive effects of the current economic environment given that businesses looking to improve cash flows often turn to financing as a potential solution. As well, inflation tends to be positively correlated with demand for real assets given that the revenue generated by equipment rises during inflationary periods. This will further increase the demand for equipment financing.

However, there are also some negative effects of an inflationary environment, such as the slowdown of key sectors, such as construction. This could cause some specialized equipment finance companies to struggle, which may lead to some consolidation in the space.

Recent transactions in this space include Peoples Bancorp’s acquisition of Vantage Financial (closed on March 7, 2022), for $54 million (full article here) and TimePayment’s acquisition of Diversified Capital Credit Corp (closed on January 25, 2022), for an undisclosed amount (full article here).

Impact on Debt Collection Agencies

Higher interest rates and higher prices lead to increased defaults – both for consumers and firms – which should drive increased business for collection agencies. Rising costs due to high inflation may also reduce liquidity for some companies, which could lead them to sell their accounts receivables to debt collection agencies sooner than usual, when debts may be easier to recover.

The collection agency industry is highly fragmented with over 3,200 collections agencies across the U.S., although increased regulation has led to consolidation, specifically Regulation F (or ‘Reg-F’) which, due to high compliance costs, is pushing small firms to be sold. The increased business costs present in today’s economic environment could further increase consolidation.

Recent transactions in this space include Complete Recovery’s acquisition of Prince Parker (completed on March 1, 2022) – its second acquisition in three weeks (full article here), and First Source’s acquisition of American Recovery Service for $53 million on December 29, 2021 for $53 million (full article here).

CONCLUDING REMARKS

While certain areas in our coverage verticals are experiencing more pressure than others, our research points to an economic outlook that is relatively stable within a well-functioning financial system. For CEOs and Founders who are looking to kick off a transaction process this Fall, we foresee much of the COVID crash to be worn off by mid to late 2023, with transaction dynamics normalized (short of another pandemic or large military scale invasion) by this time.

Figure 1. Federal Funds Rate, Jan 2017 – August 2022

Figure 2: Correlation between Interest Rates and Excess Returns of Actively Managed Funds

Figure 3: Bank Loan to Deposit Ratios